Crummy 2019 Earnings to Thunder Back This Year, Seers Say. Uh, Really?

Unexciting economic growth and the Chinese virus are among the ills that could ruin predictions of an electrifying rebound.

Wow, a blitz of good corporate earnings is on the way. Or not. This buzzy prospect may end up grounded out.

Sure, to listen to analysts, corporate earnings are due for a turnaround this year after a punk 2019. Analysts, pointing to positives like the truce in the US-China trade war and still-strong American consumer spending, figured that the profit picture will grow brighter as 2020 progresses.

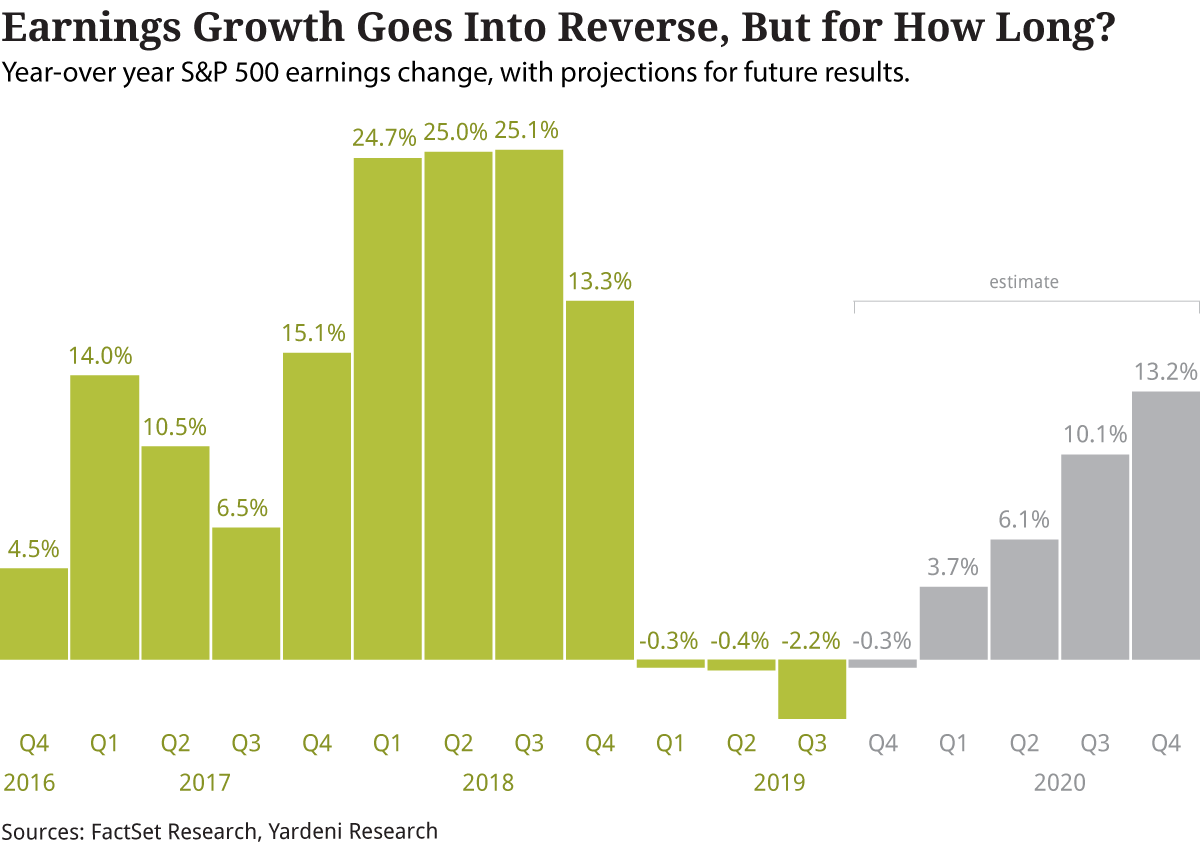

But will it? What would prompt companies to log appreciably better earnings after 2019’s blah performance? For last year’s fourth quarter, with almost half the S&P 500 companies already reported, the consensus is for a slightly down showing (negative 0.3%), which makes last year basically flat, according to FactSet Research.

Regarding 2020, though, the S&P 500 outlook becomes downright flashy, with earnings increases accelerating every quarter, starting with a 3.7% gain in the first period and ringing out the finale at a 13.2% rise, for an overall yearly tally of 9.1%.

Quite a comeback, considering that US economic growth slowed to 2.3% in 2019 from 2.5% the year before. Forecasts for 2020 are similarly unspectacular. What’s more, optimism about a better 2020 seem problematical if the growing coronavirus in China manages to choke off the output of the world’s second largest economy.

Looking at the turnaround projections, William Dellwiche, a Baird investment strategist, commented, “That’s a whole lot of optimism without a lot of optimism in the economy.” Analysts tend to be sanguine about the future as a rule, he said, and become less so as time goes by, meaning some of these rosy scenarios might become less alluring. “It’s a big dance.” We’ll only really have a good idea at this year’s mid-point, he added.

Earnings Ups and Downs

The earnings story since the Great Recession has been erratic, Yardeni Research data indicate, as the US and the world climbed out of a slough of despond amid fears that the bad times would reappear soon. In 2010, the first full year after the recession, a nice 40.3% increase showed up. After that, earnings growth moderated, with a string of mid-single digit boosts.

Then, profits fell into a pit again during the 2015-16 mini-recession. This slump, which technically did not constitute an actual recession as gross domestic product didn’t quite turn negative, resulted from a crash in oil prices and a Chinese economic slowdown

The picture improved by late 2016 and into 2017, the first year of the Trump Administration (earnings up 11.8%), with talk of lighter business regulations and corporate tax cuts. The tax reduction, to 21% from 35%, proved to be a bonanza for US companies when it took effect in 2018. Earnings expansion swelled 22.7%.

So, that made the 2019 fall-off more disappointing. Many market observers label the 2018 jump as a “sugar high,” pleasing yet temporary as a general economic unease took hold. While the long-term effects of the tax reduction remain debatable—the new law did make US tax rates more competitive with those of foreign competitors—it hasn’t provided much fuel lately.

Some reports during the current earnings season look pretty good. Apple, for instance, saw fourth-quarter profits return after a tumble in iPhone sales, posting $22.2 billion amid record sales that included renewed interest in the iconic smartphones. The unknown here is China’s situation. China accounts for almost a fifth of Apple’s revenue and assembles most of the iPhones, iPads and Macs it sells all over the earth.

The Case for Profit Pessimism

Virus scares have harmed stocks during the past two decades, with the S&P 500 dropping between 6.9% and 12.9%, depending on the epidemic, a Citigroup report found. What’s frightening about these outbreaks is that they might become Black Plague-like scourges that kill millions and slam the world economy, as happened in the 1918 Spanish flu outbreak.

The last time China suffered a virus upheaval was in 2003, when SARS, or severe acute respiratory syndrome, sickened almost 90,000 and killed 774. But China at the turn of the century was a much smaller player on the global economic scene. The international impact of SARS was small and fleeting.

Now, the landscape has changed. China is a hub of worldwide manufacturing, a vital link in the global supply chain, and a huge buyer of goods and services that other nations rely on for sales. If it remains closed for business, with many work sites silent and air travel from abroad slashed, the damage could become far worse.

More broadly, the GDP outlook for major developed countries, which are the US’s main trading partners, is hardly soul stirring. For Deepak Puri, CIO Americas at Deutsche Bank Wealth Management, 2020’s estimated earnings “rebound seems unrealistic, given the expected continuation of the macroeconomic slowdown.”

The International Monetary Fund has projected 2.4% GDP growth this year for the US, in keeping with the country’s ho-hum post-recession record. The IMF has a similarly uninspiring view for the rest of the developed world, with 1.2% projected for Germany, 1.4% for Britain, and 0.5% for Japan. The European economy has slowed markedly, with the 28 countries in the European Union expanding only 0.1% in the fourth quarter, versus the previous period.

A majority of CEOs, 53%, forecast a drop in the economic growth rate for 2020, according to consultants PwC. That’s the highest pessimistic score since the consulting firm started asking this question in 2012. In 2019, 29% of CEOs expected a decline in the pace of economic growth; in 2018, it was 5%. To be sure, the 2020 survey 1,600 CEOs from 83 countries answered before the announcement of the phase one deal halting the Sino-American trade war.

One worry CEOs have is rising wages due to a tight labor market, with a mere 3.5% unemployment rate in the US. Wages increased at a 3.7% clip last month, almost triple the raises granted 10 years before. “Corporations are getting squeezed with wages,” Baird’s Dellwiche said. “And wages are outpacing productivity.” Indeed, the most recent 12-month increase in productivity, ending September 30, was 1.6%.

A lot of the earnings heroes lately are tech giants like Apple. This group tends to score well in the profits arena, with the likes of Amazon and Microsoft turning in strong reports recently. Financial services are having a good time these days, too. JPMorgan Chase announced a 21% earnings bump. Even long-suffering General Electric managed to turn in good numbers for a change.

Alas, the motley crew of earnings laggards is taking the shine off these stars. Chief offender: Boeing, with its ongoing agony over the grounded 737 Max, its top product. The plane maker last week reported its first loss since 1997, what with the return of the MAX delayed until mid-year, if not later.

Meanwhile, the oil patch is suffering thanks to low crude prices. Industry leader Exxon Mobil’s earnings were down 5% in the last quarter. Manufacturing is another problem area. The sector contracted for the fifth month in a row as of December’s end. Industrial conglomerate 3M, which makes everything from Post-Its to power cables, suffered a net income dip of 28% last quarter.

The Case for Bottom Line Buoyancy

If the past is any guide, the coronavirus should peter out before inflicting any lasting impairment to the world economy. “A virus like this will last three to four months, as people in China hide in their houses,” said Doug Foreman, CIO of Kayne Anderson Rudnick Investment Management. “But it’s transitory.”

To John Augustine, CIO of Huntington Private Bank, the virus likely will shave a half-point off S&P 500 earnings growth this year, which should end up rising 8.5%. “Earnings and the economy will pause, then come back,” he said. Augustine said the SARS virus “made us lose a few months, then we recovered that.”

In addition, there’s the economic spur in the US and abroad from central banks. After hiking interest rates after a decade at close to zero, the Federal Reserve did a U-turn last year and lowered three times, and also began buying assets again, known as quantitative easing, or QE. “You won’t see them going higher in 2020,” said Brian Kessens, a portfolio manager at Tortoise, noting that a reelection-minded President Donald Trump has pressured the Fed to bring them down even more. “That’s a big stimulus.”

At the same time, the European Central Bank has pushed rates further into negative territory and also revived its QE program. In fact, the IMF announced that global growth in 2019 and 2020 would be 0.5 percentage point lower without the central banks’ help. And Erica Bergsland, senior vice president at Securian Asset Management, noted that an easing monetary policy takes a while to kick in, hence its full effect has yet to be fully realized.

Despite some remaining headwinds, emerging markets nations should generate decent GDP improvements in 2020, according to the IMF, which expects 3.3% global growth, compared to 2.9% last year. EMs should be up 4.6% this year, the agency believes. Makes sense: Emerging nations compose an increasing share of the global economic pie.

Absent a recession, “beaten-up sectors, like energy and industrials, are likely to see a rebound in 2020, even without a big upturn in economic growth,” observed Securian’s Bergsland. The reasoning is that so-so economic growth might be sufficient to stabilize such laggards, and any hint of better earnings will appear strong because 2019’s comparable readings were lousy.

Aside from the recent price slides from virus heebie-jeebies, the stock market has taken the rocky earnings of 2019 in stride. If 2020 doesn’t live up to its hype, that market sunshine may dim.

Related Stories:

3rd Quarter Earnings Are Down, but not as Much as Expected

Analysts: Earnings Will Improve in 2020

The S&P 500 Keeps Singing the Sour Earnings Song