Fixed income, diminished yet unbowed, still occupies an important if sometimes underwhelming place in institutional portfolios. Time was, bonds and their ilk provided ballast during stock market upheavals, as well as income and price appreciation.

It seems all that’s left is ballast. “Broadly speaking, fixed income still plays the ballast role,” said Lon Erickson, a portfolio manager at Thornburg Investment Management. “We saw that last year.”

Recall back in dreaded 2020 when stocks skidded toward the drain and then recovered mightily. Fixed income securities, after some sickening gyrations of their own in March, held up. Defaults weren’t as bad as feared. Moreover, some parts of the fixed income universe still can deliver appreciation and income, although more modestly than before.

Nowadays, bonds often are the stepchildren in many institutional portfolios. At the South Dakota Investment Council (SDIC), CIO Matt Clark keeps a chunk of fixed income: 23% investment grade, 7% high-yield, as of the most recent report ending mid-year 2020. Just the same, he is no fan of the current fixed income climate, saying, “An investment in bonds may earn you 1% to 2%, but it would earn zero if rates drift up.”

And bonds often are less preferable than cash, in Clark’s view. “Cash is superior to bonds as a diversifier if rates are biased to increase,” he said. As a value investor, he always is looking for stock opportunities, which he finds money stashed into bonds is less able to deliver than cash. “Cash can be more liquid, to allow rebalancing into risky assets in a crisis,” he argued. Sometimes, he has as much as 30% cash on his books, ready for deployment.

Twenty years ago, bonds were almost one-third of public pension plans’ holdings, at 31.5%. As of 2019, that had shrunk to 23.2%, according to the Public Plans Database. This drop-off, of about a quarter, likely continued last year.

The push is on at many public funds to grow their deficient funded statuses. The answer for them often lies with equity and alternatives, known as alts, such as real estate, private equity, and hedge funds.

Fixed income gets somewhat better treatment from corporate defined benefit (DB) plans, which tend to be better funded. Companies are aggressive about de-risking, through lowering their stock exposure. Along the way, they have notched up their ownership of good old reliable bonds by a small amount over the past year, to 43% from 39%, a Conning study shows.

Lately, fixed income has benefited from a trump card. Bonds have had the assurance that the Federal Reserve is their backstop, with a commitment to buy investment grade corporates and fallen angels, namely bonds that have tumbled into speculative territory. This guarantee has elapsed, yet no one doubts it could be quickly brought back if needed.

The biggest bugaboo for fixed income investors, aside from a credit quality decline, is inflation, which would usher in higher interest rates and price drops. But right now, inflation isn’t much of a concern: The Consumer Price Index (CPI) last month rose 1.4% year over year, in keeping with recent history.

Still, the bond market expects some modest inflation increase ahead amid a pandemic recovery and more federal stimulus. That’s why yields on 10-year Treasury notes, the fixed income benchmark, have crept up to 1.1%, from 0.5% in the dark days of March.

“Inflation keeps me up at night,” said Robin Diamonte, CIO of Raytheon Technologies, whose retirement plans have $110 billion in assets. “Not because it’s in my base case for what’s going to happen, but because we haven’t had inflation in quite a while.” If the consensus expectations for mild inflation are wrong, she has some strategies to counter that.

Bonds Get Benched

How times have changed. The great bond rally is over, done in by Federal Reserve-mandated low interest rates aimed at combating the current and the last recession, and the slow economic growth in between.

The rally started after Paul Volcker’s Federal Reserve defeated chronically high inflation in the early 1980s: Bonds racked up double digit returns for the next two decades and then some.

When fixed income yields came down from their inflation-juiced levels, bond appreciation blossomed, recounted Jim Robinson, who manages the Liberty Robinson Tax Advantaged Income Fund and the Liberty Robinson Opportunistic Income Fund. Yields and prices move in opposite directions. “The starting yields were very high,” he said.

Since the aughts, bond price appreciation has been tepid amid contracting yields, and total returns (price growth plus interest income) have dropped with them. The Bloomberg Barclays US Aggregate Bond Index, aka the Agg, has settled down to generally low single-digit gains yearly.

The yields are nothing special these days, with 10-year Treasuries at 1.1%, and investment grade corporates and mortgage-backeds a mere 0.8 percentage point higher. Junk bonds, at an average 4.3%, are about half what they were in the beginning of 2019.

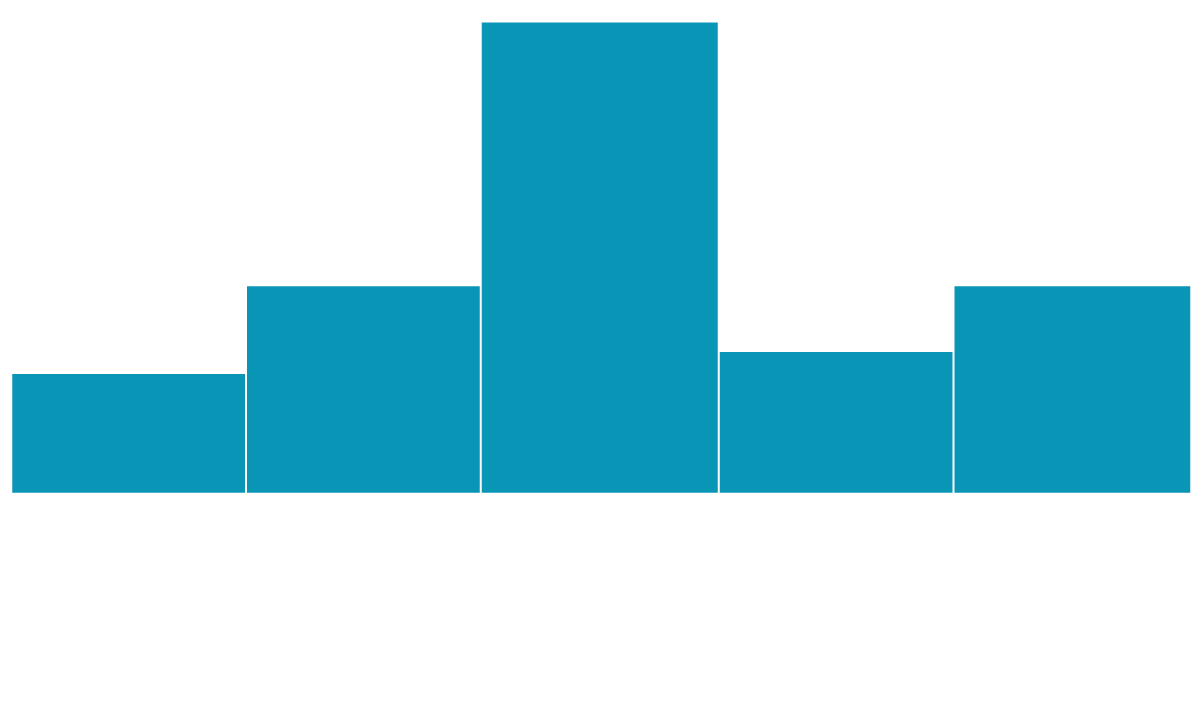

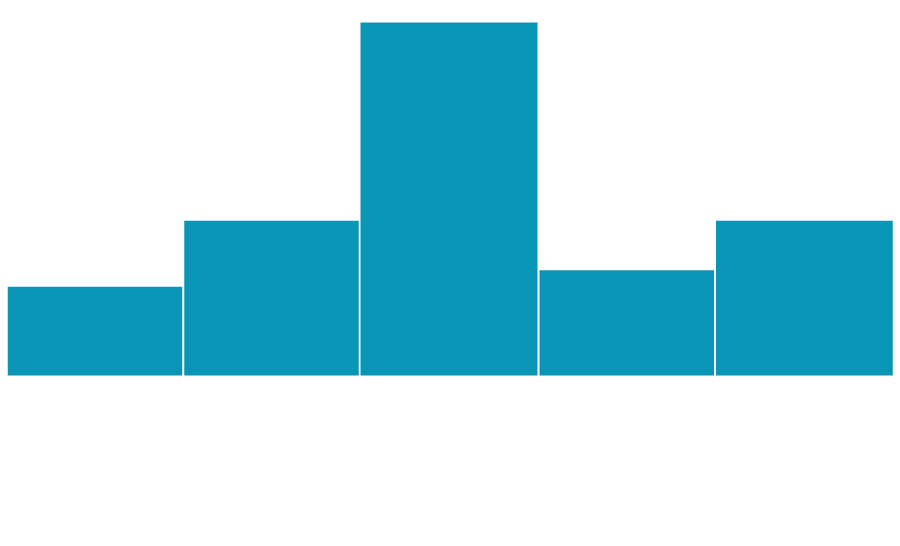

Fixed Income: Not a Lot of Income Here

Yield as of January 19, 2021, except for CLOs, which are year-end 2020

4.3%

1.9%

1.9%

1.3%

1.1%

Mortgage-Backed Securities (MBSs)

Collateralized Loan Obligations (CLOs)

10-Year

Treasuries

Investment Grade Corporate Bonds

Junk Bonds

Sources: Yahoo Finance (Treasuries), ICE Data Services (investment grade and junk bonds), Fannie Mae (MBS), S&P Global Ratings (CLOs)

And yet … “Fixed income still has a core role,” said Matt Daly, managing director of corporate and municipal teams at Conning. And, occasionally, sharp managers can zero in on gems, he added. “Bonds issued in March and April,” he said, referring to when fixed income was in a tailspin last year, “have appreciated a lot.”

Despite their diminished capacity, bonds have fulfilled their duty as a portfolio ballast in recent years. In the scary days of 2008, when the S&P 500 plunged 38.5%, the Agg was up 5.2%. In 2018, when rising rates pushed stocks to a 6.2% loss, the Agg was flat.

And then there’s 2020, as panic pushed almost everything down in spring, with a hopeful bounce back following. The S&P 500 finished last year ahead 16.3%, and the Agg came in at 7.5%—not spectacular for bonds, but not shabby either.

A Foray Through Fixed Income

Let’s take a glimpse at the outlooks for the major asset categories in fixed income:

Treasuries. If indeed somewhat higher rates are coming this year, a development that’s never great for bond prices, then investors can take comfort that the Federal Reserve will be on hand to buy heavily, helping Treasury prices. The trouble is that Fed purchases have tilted toward the shorter end of the yield curve.

That has left the benchmark 10-year note more subject to the whims of the market, which these days is convinced that a whiff—just a whiff, mind you—of inflation is in the wind. For that reason, the Charles Schwab brokerage believes that the yield on the 10-year could range as high as 1.6% this year. Some think it will go higher still. Recall that just two years ago the 10-year bond yielded 3.1%.

Expect no shortage of Treasury issuance ahead. Massive pandemic relief plans from the Biden administration would bring a cornucopia of deficit spending. “I feel that we can afford to do what it takes to get the economy back on its feet,” Treasury Secretary-designate Janet Yellen told a Senate committee on Tuesday. Republicans in Congress are skeptical about what they term a spending blowout.

Investment Grade Corporates. As Garrett Tripp, portfolio manager of Braddock Multi-Strategy Income Fund, sees these, “Their low yield makes it tough to get appreciation—and they don’t provide the income I need.”

A possible upward rate movement will do investment grade bonds no favors. Duration (which measures the susceptibility of bond prices to rate changes) is on the high end for these bonds, averaging 8.5 years. Thus, if rates rise 2 percentage points in the next couple of years, the bonds would lose 17% in price.

For the moment, the average corporate credit spread for US Treasuries and investment grades is a tight 0.97 point. CreditSights, the independent research firm, has downgraded this segment to underperform from outperform. While default risk is small, the spread to Treasury paper is too narrow to offer much in the way of extra interest over Treasuries. Over the past two decades, investment grade spreads have been lower than now only about 15% of the time, by the calculations of research firm Morningstar.

The good news is that investment grades, which saw rampant issuance last year due to low rates, are expected to have fewer new entrants this year. That should help support prices. Corporations are awash in cash, making the need to raise more capital less pressing, particularly if the economy expands nicely, post-coronavirus.

We’ll see: Investment grade issuance remains robust in January, with John Deere (selling $1.5 billion in bonds) and Home Depot ($3 billion) leading the charge.

Junk Bonds. These creatures are far from the pariahs they were in the early 1990s, when many blew up owing to over-leveraged issuers’ folly. Of late, junk has been in demand for its relatively large interest coupon, which makes the bonds pricey.

The average price for high-yield is 105 cents on the dollar, by the measure of the Bloomberg Barclays US High Yield Index. And to many investors, the bonds don’t seem very risky. To wit: The credit spread for junk is a mere 3.77 points, which is far down from 5-point gap back in March.

Duration has been lower with junk: On average it’s just 3.7 years. Hence, a 2-point rate increases loses only 7.4% in price. That’s because junk has shorter effective maturities. While high-yield bonds are typically issued with 10-year terms, they are often callable after only a few years. Amid the low rates of recent years, many issuers bought back their junk bonds, which could be re-issued with lower coupons. If rates do inch back up, though, that situation won’t prevail.

A spate of fallen angels—investment grade-rated credits downgraded to speculative status—took place in 2020, with 1,800 companies landing in junk land. That was a nine-fold increase from 2019. The good thing is that a number of these demotions, to junk from BBB, the last investment grade, were of companies with good balance sheets and strong resources, such as Kraft Heinz.

A big question in this realm is what will happen should the pandemic and its attendant economic downturn not recover as soon as Wall Street expects. Then, high-yield paper from leisure, travel, and gaming would suffer, noted Jim Schaeffer, global head of leveraged finance at Aegon Asset Management.

Junk defaults doubled to 8.4% as of November, from the year before, by the count of Moody’s Analytics. That, however, was far lower than original predictions: Many had projected defaults to be in the mid-teens in the current recession.

Mortgage-Backed Securities. In spite of early-2020 fears that the pandemic would propel the US housing market back into a 2008-style abyss, residential real estate has done well. Low rates, constrained supply, and savings-heavy consumers are the reason. In this K-shaped recession, folks on the lower end of the economic spectrum haven’t fared as well, but those on the other side have.

Those fortunate souls are the homebuying population. Mortgage defaults are low. “The consumer is in a good place and the collateral is good,” said Erickson, the portfolio manager at Thornburg Investment Management. Ergo, mortgage-backed securities (MBSs) have done well. Over the past 12 months, the S&P US Mortgage-Backed Index is up almost 4%.

Of course, one huge tailwind for MBSs is that the Federal Reserve has been buying them up since March, to the tune of $40 billion per month (along with twice that amount for Treasury bonds). This effort, known as quantitative easing, or QE, puts downward pressure on interest rates, and it will end at some point. The Fed has given no signal when that might occur, so odds are QE will be around for a while.

One advantage for MBSs is that they don’t get hurt badly on prices when rates rise. On average, the duration of agency-backed mortgage bonds is low—around three years—likely due to borrower re-financings of their underlying home loans. So, if rates go up 2 percentage points, MBS prices fall just 6%. Also helping out is that mortgage delinquency is not large, 7.6% as of last year’s third quarter, about twice what it was 12 months prior, but still on the downswing from the April-June period.

Leveraged Loans/Collateralized Loan Obligations. These were enjoying bountiful issuance after the first COVID-19 wave, and have ebbed a bit since with the current virus onset. Defaults increased to 4% of volume in late October, four times the level from 12 months before. But a big positive is that their duration is very, very low, at three months, Braddock’s Tripp indicated. And they have a floating rate—usually LIBOR plus 4 percentage points or so. For issuers, that’s a salubrious attribute (provided rates don’t spike, which is unlikely nowadays).

Overall, leveraged loans (bank lending to highly indebted companies) have surged this century, despite slumps during the 2008 financial crisis and in early 2020, amid the advent of the pandemic. In 1998, the junk bond volume overshadowed that of lev loans, 7 to 1. By 2010, loans were about half the size of junk. Most recently, they were close to parity.

Packaged into collateralized loan obligations (CLOs), loans are now a firm part of the capital structure. And especially as funding mechanisms for mergers and acquisitions (M&A), which have bounced back from last spring’s black hole. Most forecasts have the M&A trend continuing, good news for leveraged loan issuance. A boom in warehouses, thanks to all the online ordering of goods, should help drive that further, Aegon’s Schaeffer said.

Upshot: Bonds can dependably deliver, even if it’s not as much as they used to give. The first recorded bond in history was around 2400 BC, in ancient Mesopotamia. It paid interest in grain. This year, some may think bond interest is similarly uninspiring. The truth remains that bonds have long endured, because of a promise that they have, for the most part, kept.

Related Stories:

Special Report: How Private Credit, Subject of Scary Forecasts, Came Out a Winner

Special Report: Why Pennsylvania SERS is Moving Toward a Liability-Driven Benchmark

Dalio Says Holding Government Bonds Now Is ‘Crazy’

Biden Tax Hikes Would Help Junk Bonds, Says Market Savant

Tags: appreciation, ballast, Bonds, cash, CLOs, corporate defined benefit plans, Federal Reserve, Fixed-Income, income, Interest Rates, investment grade corporate bonds, Junk Bonds, leveraged loans, Matt Clark, mortgage-backed securities, Public Pension Plans, Raytheon Technologies, Robin Diamonte, South Dakota Investment Council, Special Report Fixed Income 2021, Treasuries