The Rhode Island State Investment Commission has approved a new measure that would allow it to purchase secondary interests in LP fund commitments, with the purpose of allowing the commission more flexibility to build out its private growth portfolio to align with its new 15% target.

The commission said it expects its private growth segment to be the “overall portfolio’s highest return generator over the long term,” so it extended the target from its previous 6.5% in 2016 to become a more robust investor in the space, subsequently stimulating approval of the new secondary investment approach.

It would allow the institution to be more diversified in terms of sector and geography, a spokesperson told CIO, part of which is necessary since there’s a relatively heavy allocation to buyout strategies in the portfolio. It’s been the best-performing asset class to date (net of fees) over most time horizons.

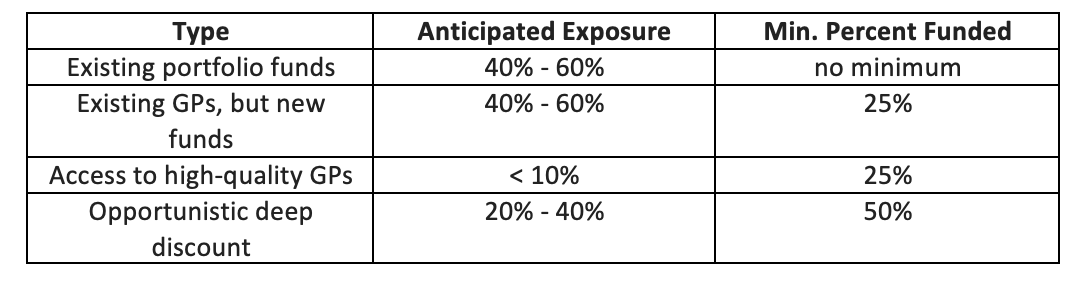

The recently implemented pacing plan calls for about 10 private equity commitments per year, with each being between $20 million to $60 million, the spokesperson added, during what is said to be a contemporary “five-year ramp-up” period. The portfolio’s anticipated composition is illustrated here:

“Many high–quality funds are hard to access,” Rhode Island said. “If [the commission] is able to get into such a fund via a secondary transaction, that can be an alternative way to gain such exposure. Additionally, GPs prefer to have consistent investors across fund vintages so the secondary may provide access to new funds with the high–quality GP on a primary basis.”

The commission also discussed the possibility of capitalizing on certain situations where an LP may be forced to liquidate its positions at deep discounts. “These may not be funds [the commission] would commit to on a primary basis, but the discount on the current portfolio and potential upside of the unrealized investments is attractive enough to warrant investment,” it said.

Overall, the institution is doing generally well with its $287 billion portfolio, having just recently outperformed its 3.60% benchmark and pulling in 4.14%, earning the fund $323 million. The returns were mostly fueled by the fund’s investments in the global stock market, which were mostly low-fee index funds.

The fund is currently leading a class action lawsuit against Google for failing to disclose security breaches the Google Plus social media platform had executed.

Related Stories:

Rhode Island Pension Beats Benchmarks

Rhode Island Retirement to Lead Class Action Lawsuit against Google